All Categories

Featured

Table of Contents

That normally makes them a much more budget-friendly option for life insurance coverage. Some term policies may not maintain the premium and fatality benefit the exact same in time. You don't intend to incorrectly believe you're purchasing degree term coverage and after that have your fatality advantage change later. Numerous people get life insurance policy protection to aid monetarily protect their liked ones in case of their unforeseen death.

Or you might have the choice to transform your existing term coverage into a long-term plan that lasts the remainder of your life. Numerous life insurance coverage policies have potential advantages and drawbacks, so it's vital to comprehend each before you decide to buy a plan.

As long as you pay the costs, your beneficiaries will certainly get the survivor benefit if you die while covered. That claimed, it is essential to note that a lot of policies are contestable for two years which suggests protection can be rescinded on fatality, needs to a misrepresentation be found in the application. Plans that are not contestable typically have actually a rated death advantage.

Costs are typically less than entire life policies. With a level term plan, you can choose your protection quantity and the plan size. You're not secured right into an agreement for the remainder of your life. Throughout your plan, you never have to bother with the costs or survivor benefit quantities changing.

And you can't squander your policy throughout its term, so you will not get any type of financial take advantage of your previous coverage. Similar to other kinds of life insurance policy, the expense of a degree term plan depends upon your age, insurance coverage requirements, employment, way of living and wellness. Normally, you'll find a lot more budget friendly protection if you're younger, healthier and much less dangerous to guarantee.

A Renewable Term Life Insurance Policy Can Be Renewed

Given that level term costs stay the very same for the period of insurance coverage, you'll recognize specifically how much you'll pay each time. That can be a large aid when budgeting your expenses. Level term insurance coverage also has some versatility, enabling you to tailor your plan with added functions. These typically come in the form of cyclists.

You may have to fulfill specific problems and qualifications for your insurance firm to establish this cyclist. There likewise could be an age or time limitation on the protection.

The survivor benefit is commonly smaller sized, and coverage normally lasts up until your youngster turns 18 or 25. This rider may be a much more cost-efficient means to assist guarantee your kids are covered as bikers can often cover multiple dependents simultaneously. As soon as your kid ages out of this coverage, it might be feasible to transform the biker into a brand-new plan.

The most typical type of irreversible life insurance is whole life insurance, however it has some key distinctions compared to level term coverage. Right here's a basic review of what to consider when comparing term vs.

Comprehensive Annual Renewable Term Life Insurance

Whole life insurance lasts insurance coverage life, while term coverage lasts insurance coverage a specific period. The costs for term life insurance coverage are generally lower than entire life protection.

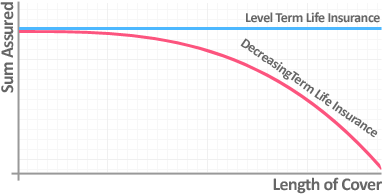

Among the highlights of degree term insurance coverage is that your costs and your death benefit do not change. With reducing term life insurance policy, your costs stay the very same; nevertheless, the death advantage amount gets smaller in time. As an example, you may have coverage that begins with a death advantage of $10,000, which can cover a home mortgage, and afterwards annually, the survivor benefit will certainly lower by a set amount or portion.

As a result of this, it's typically a more economical sort of level term protection. You may have life insurance with your company, but it might not suffice life insurance policy for your needs. The initial step when acquiring a plan is identifying exactly how much life insurance you need. Take into consideration variables such as: Age Family size and ages Work standing Revenue Financial obligation Lifestyle Expected last expenditures A life insurance policy calculator can assist identify just how much you need to begin.

After determining on a plan, complete the application. For the underwriting process, you may need to give basic individual, health and wellness, way of life and work information. Your insurance company will identify if you are insurable and the threat you may offer to them, which is mirrored in your premium costs. If you're approved, authorize the paperwork and pay your initial premium.

Trusted Does Term Life Insurance Cover Accidental Death

Take into consideration scheduling time each year to assess your plan. You may intend to upgrade your beneficiary details if you have actually had any kind of considerable life changes, such as a marriage, birth or divorce. Life insurance policy can sometimes really feel challenging. You do not have to go it alone. As you explore your alternatives, take into consideration reviewing your requirements, desires and worries with a monetary professional.

No, level term life insurance coverage does not have cash value. Some life insurance policy policies have an investment feature that allows you to construct money value in time. A part of your premium payments is reserved and can earn passion with time, which expands tax-deferred during the life of your insurance coverage.

These plans are commonly considerably much more pricey than term coverage. If you get to completion of your plan and are still to life, the protection ends. You have some choices if you still want some life insurance protection. You can: If you're 65 and your coverage has run out, for instance, you might intend to buy a new 10-year level term life insurance coverage plan.

Premium What Is Direct Term Life Insurance

You may have the ability to convert your term protection into an entire life policy that will last for the rest of your life. Lots of kinds of degree term plans are exchangeable. That indicates, at the end of your protection, you can transform some or every one of your plan to entire life coverage.

Level term life insurance is a policy that lasts a collection term normally in between 10 and three decades and includes a level survivor benefit and degree costs that stay the very same for the whole time the policy holds. This means you'll recognize precisely how much your settlements are and when you'll need to make them, permitting you to spending plan as necessary.

Level term can be a fantastic alternative if you're wanting to buy life insurance policy coverage for the very first time. According to LIMRA's 2023 Insurance Barometer Study, 30% of all grownups in the U.S. need life insurance policy and don't have any sort of plan yet. Degree term life is predictable and inexpensive, which makes it among the most prominent kinds of life insurance policy.

{kind=link}

Latest Posts

Best Annual Renewable Term Life Insurance

Trusted Level Premium Term Life Insurance Policies

Irish Life Mortgage Protection Quote